*”Nearly 64% of Americans live paycheck to paycheck.”* — That stat alone should make every one of us sit up straighter. So when life throws a $300 surprise at you before payday, what do you do?

You scramble. You stress. You might even consider a payday loan — Now you know that you don’t have to do it, or at least after reading our Cash Advance Apps Guide.

Here’s the good news: cash advance apps exist for exactly this moment. And two of the biggest names in the space are **Earnin** and **Dave**. Both promise fast cash, low (or no) fees, and a financial lifeline when you need it most. But they’re not the same. Not even close.

So which one is actually worth downloading? In this **Earnin vs Dave** breakdown, we’re going deep. No fluff, no filler — just the real comparison you need to make a smart decision. This article is part of our **Ultimate Guide to Cash Advance Apps**, and it’s designed to give you everything a standalone review can’t.

Let’s get into it.

What Are Cash Advance Apps and Why Does the Earnin vs Dave Debate Even Matter?

The Rise of the Payday Alternative

Cash advance apps — sometimes called earned wage access apps or payday advance apps — let you borrow a small amount of money against your upcoming paycheck. No credit check. No predatory interest rates. No awkward conversation with your bank manager.

They emerged as a direct response to the payday loan industry, which has long trapped low-income workers in cycles of debt with APRs that can exceed 400%. That’s not a typo. Four. Hundred. Percent.

Cash advance apps flipped the model. Instead of charging outrageous interest, most charge small flat fees or rely on optional tips. It’s a genuinely better system — but only if you pick the right app for your situation.

That’s exactly why the Earnin vs Dave question matters so much.

Who Are These Apps For?

Both Earnin and Dave target working adults who occasionally need a small financial bridge. Think of situations like:

- Your car needs a repair that can’t wait

- A utility bill is due two days before payday

- You’re short on groceries after an unexpected expense

- You need a little cushion to avoid an overdraft fee

Sound familiar? Then this Earnin vs Dave comparison was written for you.

Earnin vs Dave: A Quick Overview Before We Dive Deep

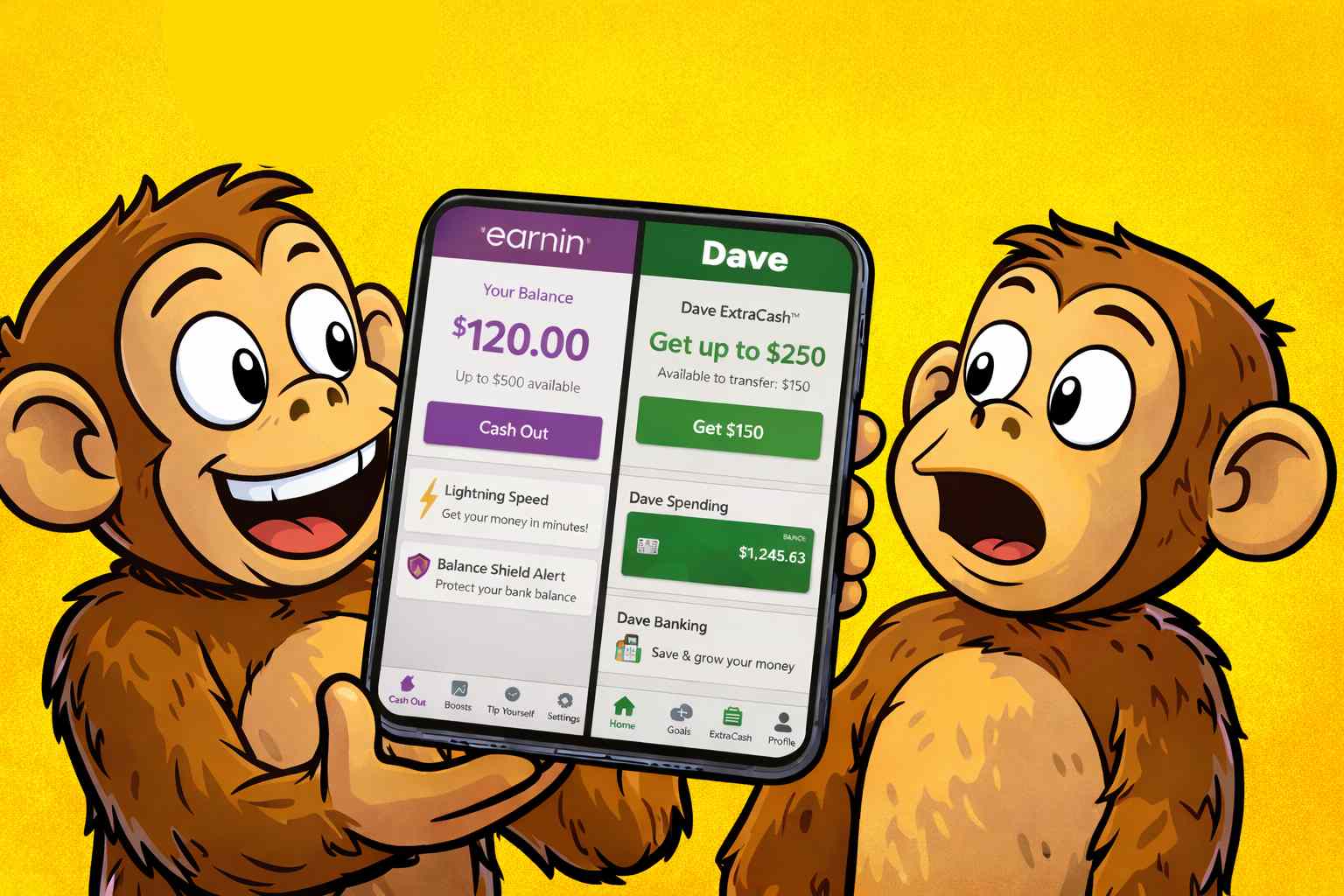

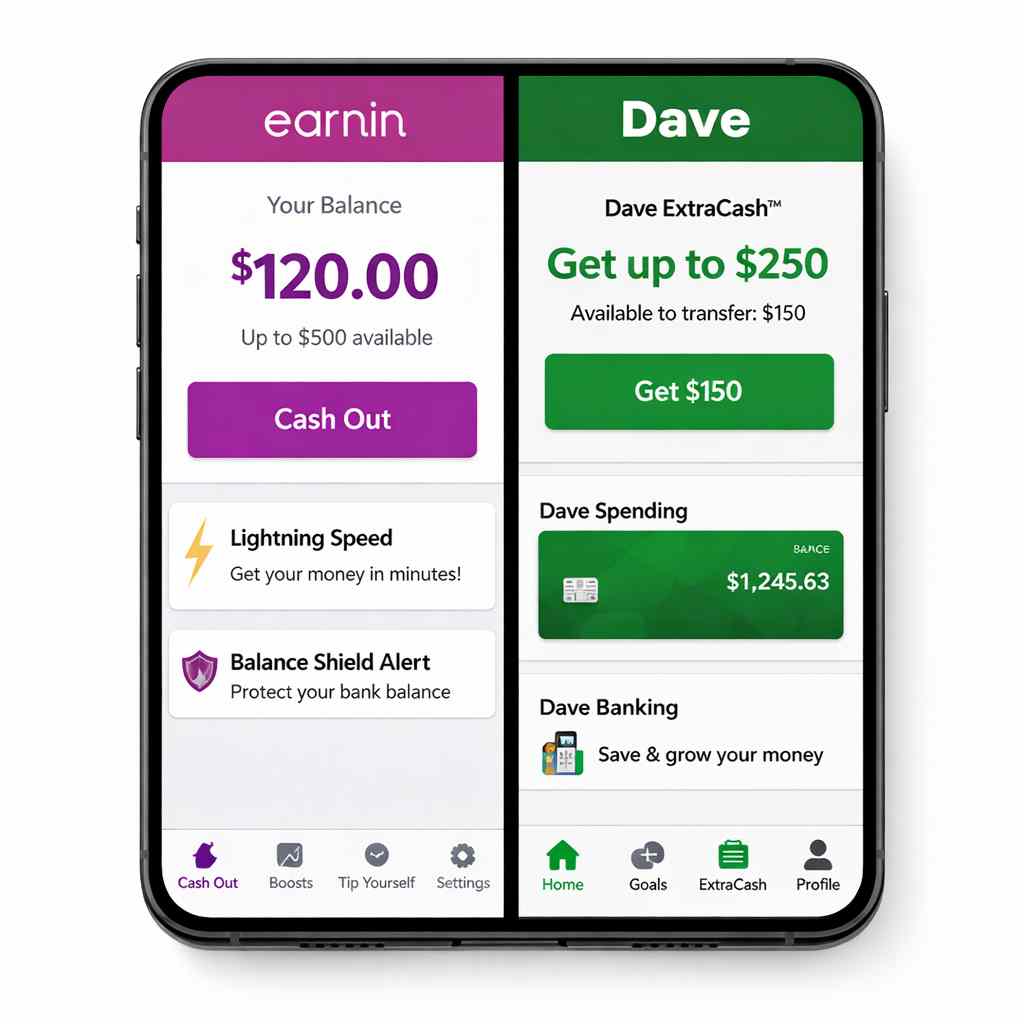

What Is Earnin?

Earnin is a cash advance app that lets you access money you’ve already earned — before your employer pays you. Founded in 2013, it’s one of the oldest players in this space. The core premise is simple: you work today, you get paid today. Not in two weeks.

Earnin connects to your bank account and verifies your employment and earnings. Based on that data, it gives you access to a portion of your earned wages on demand. There are no mandatory fees. Instead, Earnin uses a “pay what you think is fair” tip model.

What Is Dave?

Dave launched in 2017 and quickly became one of the most downloaded personal finance apps in America. Like Earnin, it offers cash advances — but Dave bundles them with a fuller suite of banking features. Dave charges a $1/month membership fee and offers advances through its ExtraCash™ feature.

Dave also has a built-in budgeting tool and even offers a spending account with a debit card. It’s less of a single-purpose tool and more of a mini banking ecosystem.

Both apps solve the same core problem. But the Earnin vs Dave comparison reveals some sharp differences in how they do it.

Earnin vs Dave: The Feature-by-Feature Breakdown

Cash Advance Limits — How Much Can You Actually Borrow?

This is usually the first question people ask. And rightfully so.

Earnin starts new users at a relatively low limit — typically $100 per pay period. But here’s the thing: that limit can grow. As you build a history with the app, Earnin may increase your advance limit up to $750 per pay period. That’s a meaningful ceiling if you have recurring needs.

Dave operates differently. New users can access up to $500 right away through ExtraCash™, though the actual amount you qualify for depends on your account history and direct deposit activity. In practice, many users start lower and work up.

Earnin vs Dave Advance Limits at a Glance

| Feature | Earnin | Dave |

|---|---|---|

| Starting advance limit | ~$100 | Up to $500 |

| Maximum advance limit | $750/pay period | $500 |

| Limit growth over time | Yes | Limited |

| Per-transaction or per-period | Per pay period | Per advance |

Winner: For high-limit potential, Earnin wins. For instant higher access on day one, Dave has an edge.

Fees and Costs — Where Does the Money Really Go?

This is where comparing both apps, Earnin and Dave, gets genuinely interesting. Because “no fees” doesn’t always mean what you think it means.

Earnin’s fee structure:

- No mandatory fees. Full stop.

- Optional tips ranging from $0 to $13 per advance

- Lightning Speed transfers (instant) cost $3.99

- Standard transfers (1–3 business days) are free

Here’s the honest truth about Earnin’s tip model: it works, but it relies on your goodwill. If you tip $5 every time you take a $50 advance, that’s effectively a 10% fee. That’s still far better than a payday loan, but it’s worth being aware of.

Dave’s fee structure:

- $1/month membership fee (mandatory)

- Optional tips on advances

- Express delivery (instant) costs up to $5

- Standard delivery (up to 3 days) is free

Dave is transparent. You know exactly what you’re signing up for: one dollar per month, tips if you want, and a fee for instant access. That clarity has real value.

| Feature | Earnin | Dave |

|---|---|---|

| Mandatory Fees | No mandatory fees. Full stop. | $1/month membership fee (mandatory) |

| Optional Tips | Optional tips ranging from $0 to $13 per advance | Optional tips on advances |

| Instant Transfers | Lightning Speed transfers cost $3.99 | Express delivery costs up to $5 |

| Standard Transfers | Standard transfers (1–3 business days) are free | Standard delivery (up to 3 days) is free |

| Additional Notes | Tip model relies on user goodwill. For example, tipping $5 on a $50 advance equals a 10% fee. Still generally cheaper than payday loans, but worth considering. | Requires a monthly subscription regardless of usage. |

Which Is Cheaper?

If you take one small advance per month and tip nothing, Dave costs $1. Earnin costs $0. But if you need instant access multiple times a month, the math shifts quickly. Run your own numbers based on your actual usage patterns.

In the Earnin vs Dave fee battle, Earnin wins for zero-obligation costs. Dave wins for predictability.

Transfer Speed — When Do You Actually Get the Money?

When you’re stressed and short on cash, “1–3 business days” can feel like an eternity.

Both apps offer:

- Standard (free): 1–3 business days

- Express/instant (paid): Within minutes

Earnin’s Lightning Speed costs $3.99. Dave’s express transfer costs between $1.99 and $5, depending on the advance amount. Neither is free for instant access — and that’s important to factor in.

Here’s a pro tip: if you’re using these apps regularly and always paying for express, you’re probably not using them the right way. Cash advance apps work best as occasional tools, not permanent income supplements.

Eligibility Requirements — Who Qualifies?

This is where many people hit a wall. Let’s break it down clearly.

Earnin requires:

- A regular pay schedule (hourly or salaried)

- Direct deposit to a checking account

- A consistent work location (or time-tracking for remote workers)

- A bank account that’s been active for at least 60 days

Dave requires:

- A U.S. bank account or Dave Spending Account

- Direct deposit history (boosts your eligible amount significantly)

- 60+ days of regular direct deposits for maximum access

Both apps require you to have income coming in. Neither works for the self-employed in traditional ways, though Earnin has made some progress with gig workers. If you’re freelancing or driving for DoorDash, read the fine print carefully before committing to either side of this Earnin vs Dave decision.

| Requirement | Earnin | Dave |

|---|---|---|

| Income / Work | A regular pay schedule (hourly or salaried) | Direct deposit history (boosts your eligible amount significantly) |

| Bank Account | Direct deposit to a checking account | A U.S. bank account or Dave Spending Account |

| Account History | A bank account that’s been active for at least 60 days | 60+ days of regular direct deposits for maximum access |

| Work Verification |

A consistent work location (or time-tracking for remote workers) |

No strict work location requirement, but consistent deposits are key |

Earnin vs Dave: The Extra Features Nobody Talks About Enough

Budgeting Tools

Earnin keeps it lean. The app focuses on what it does best — getting you your money early. There’s a Balance Shield feature that sends alerts when your bank balance drops below a set threshold, and an automatic advance option to prevent overdrafts. Useful! But don’t expect a full budgeting suite.

Dave goes further. The app includes:

- A built-in budget tracker

- Spending insights

- Alerts for upcoming bills

- A spending account with a debit card

If you want a more complete financial picture alongside your cash advance, Dave is the clear winner here. For people who just want early wage access and nothing more, Earnin is cleaner and less cluttered.

Banking Features

Earnin is not a bank. It doesn’t pretend to be. It connects to your existing checking account and works within that ecosystem.

Dave has evolved into something bigger. It offers a Dave Spending Account — an FDIC-insured spending account with a Visa debit card. You can use it as your primary account or as a supplement. It even offers cash-back rewards at select retailers.

This is a significant differentiator in the Earnin vs Dave conversation. If you’re looking for a financial app that can grow with you, Dave’s banking layer is worth serious consideration.

Side Hustle Job Board (Dave Only)

Dave has a unique feature called the Side Hustle job board, which connects users with gig work opportunities. It’s integrated directly into the app. Earnin has nothing comparable.

This might seem like a small thing. It’s not. Financial stress often comes from income gaps, not just timing gaps. A job board built into your cash advance app is quietly brilliant.

Earnin vs Dave: User Experience and App Ratings

What Real Users Are Saying

Both apps have millions of downloads and strong ratings. But digging into the reviews reveals some patterns worth knowing.

Earnin users consistently praise:

- The zero-fee model

- The growing advance limits over time

- The straightforward interface

Common complaints include:

- Strict eligibility requirements

- Occasional glitches with employer verification

- Customer service response times

Dave users frequently love:

- The predictable $1/month cost

- The higher starting advance amounts

- The full-featured app experience

Common complaints include:

- The mandatory membership fee (even if it’s just $1)

- Express fees feel high for smaller advances

- Some users find the app pushy with upsells

In the Earnin vs Dave user experience battle, it’s close. Dave gets a slight edge for breadth of features. Earnin gets credit for simplicity and zero mandatory costs.

This doesn’t get talked about enough. Both apps access your bank account data. That’s a significant level of trust to extend to any company.

Earnin uses Plaid (a widely trusted financial data aggregator) to connect to your bank. It collects location data (or work calendar data for remote workers) to verify employment. That location tracking raises eyebrows for some users. Worth knowing.

Dave also uses Plaid for bank connections. It collects transaction history and income data to determine advance eligibility. Its privacy policy is fairly standard for fintech, but like all apps, it does use your data to improve its services and products.

Neither app is unsafe. But both require you to share more personal financial data than a typical app. Read the privacy policies. Seriously — it takes five minutes.

Earnin vs Dave: The Real-World Scenarios

Scenario 1 — You Need $200 Right Now

You just got hit with an unexpected car repair bill. You need $200 today, and payday is six days away.

- With Earnin: You can request up to your eligible limit (possibly $200 if you’ve built history). Pay $3.99 for Lightning Speed, or wait 1–3 days for free. Tip optional.

- With Dave: Request up to $500 if eligible. Pay $3.99–$5 for instant transfer, or wait up to 3 days for free.

Verdict: Both work here. Dave might get you the money faster at a similar cost.

Scenario 2 — You’re Trying to Avoid an Overdraft Fee

Your checking account is $40 short of covering a bill. You need a small buffer, fast.

- With Earnin: Balance Shield can automatically advance money when your balance dips low. Elegant and hands-off.

- With Dave: ExtraCash™ can serve the same purpose, and the Dave Spending Account sidesteps overdrafts entirely if you use it as your primary account.

Verdict: Tie — both handle this well, in different ways.

Scenario 3 — You’re Building a Long-Term Financial Safety Net

You want an app that helps you budget, build savings, and handle occasional shortfalls — not just an emergency tool.

- With Earnin: Limited. Great for earned wage access, not much else.

- With Dave: The budgeting tools, Side Hustle board, and spending account make Dave a more complete financial companion.

Verdict: Dave wins, and it’s not close.

Earnin vs Dave: Pros and Cons Summary

Earnin: The Good and the Not-So-Good

Pros:

- Zero mandatory fees

- Up to $750 per pay period (highest potential limit)

- Grows with your usage history

- Clean, focused interface

Cons:

- Lower starting limits for new users

- Strict employment verification

- Location tracking for in-office workers

- Limited additional features

Dave: The Good and the Not-So-Good

Pros:

- Higher starting advance amounts

- Full budgeting and banking features

- Side Hustle job board

- Predictable, transparent pricing

Cons:

- $1/month mandatory fee

- Express fees can add up

- Advance limit capped at $500

- More features = more complexity

Earnin vs Dave: Which One Should You Actually Choose?

Here’s the honest answer: it depends on what you need.

Choose Earnin if:

- You want zero mandatory fees

- You’re a high earner who will eventually qualify for larger advances

- You just need a simple, no-frills cash advance tool

- You’re comfortable with optional tipping

Choose Dave if:

- You want a higher starting advance limit

- You’re looking for budgeting tools alongside your cash advance

- You want a full banking alternative built in

- You value transparency over tip-based pricing

Both apps are legitimate. Both are dramatically better than payday loans. The Earnin vs Dave decision ultimately comes down to your personal situation, your income regularity, and how much financial tooling you want in one place.

Final Thoughts on Earnin vs Dave

Cash advance apps have genuinely changed personal finance for millions of Americans. They’re not perfect — no financial product is — but they represent a massive improvement over the predatory alternatives that used to dominate this space.

Earnin is the purist’s choice. No fees unless you choose them. Clean. Focused. Grows with you.

Dave is the all-in-one choice. More features, a monthly fee, and a vision of becoming your primary financial hub.

Neither is universally “better.” Both are tools. And tools only work when you use them correctly.

For a deeper look at the full landscape of cash advance apps — including alternatives to both Earnin and Dave — make sure you check out our Ultimate Guide to Cash Advance Apps. This article is just one piece of a much bigger picture.

The right app is out there. Go find it.

Frequently Asked Questions: Earnin vs Dave

Is Earnin or Dave better for first-time users?

Dave tends to be more accessible for first-time users because it offers a higher starting advance limit (up to $500) without requiring a long account history. Earnin starts new users at around $100 and builds from there. If you need more money right away, Dave is the easier entry point in the Earnin vs Dave debate.

Do Earnin and Dave charge interest?

Neither app charges traditional interest. Earnin uses an optional tip model with fees for instant transfers. Dave charges a $1/month membership fee and optional tips, plus fees for express delivery. However, depending on how often you use these apps and how much you tip or pay for instant transfers, the effective cost can add up — so always calculate your real cost per advance.

Can I use both Earnin and Dave at the same time?

Technically yes, as long as you meet each app’s individual eligibility requirements. Some users maintain accounts with both to maximize their access to funds. However, be mindful of fees and make sure you’re not becoming overly reliant on advances as a regular income supplement — that’s a financial habit worth examining.

Which app is safer — Earnin or Dave?

Both apps are legitimate, regulated fintech products that use industry-standard security practices. They both use Plaid to connect to your bank account, which is widely trusted in the financial industry. Neither is “unsafe,” but both collect significant financial data. The Earnin vs Dave safety question is less about security and more about privacy preferences — Earnin’s location tracking is a notable consideration for some users.

Are there better alternatives to both Earnin and Dave?

Yes! The cash advance app market is competitive. Apps like Brigit, Albert, MoneyLion, and Chime’s SpotMe feature are all worth comparing depending on your situation. For a full breakdown of every major option, visit our Ultimate Guide to Cash Advance Apps — it’s the most comprehensive resource we’ve built on this topic.

This article is for informational purposes only and does not constitute financial advice. Always review the full terms and conditions of any financial app before signing up.

About the Author

Felipe is a finance and business professional with hands-on experience in credit analysis, sales strategy, and financial decision-making.

He created Monkey Money Blog to help readers understand how credit systems, financial products, and investing structures actually work — beyond marketing language and surface-level advice.