[{"id":3376,"link":"https:\/\/monkeymoneyblog.com\/apps\/how-to-instant-cash-advance-guide\/","name":"how-to-instant-cash-advance-guide","thumbnail":{"url":"https:\/\/monkeymoneyblog.com\/wp-content\/uploads\/2025\/08\/How-to-get-an-Instant-Cash-Advance.jpg","alt":"How to Get an Instant Cash Advance"},"title":"How to Get an Instant Cash Advance: Your Complete Guide to Fast Financial Relief","postMeta":[],"author":{"name":"Felipe","link":"https:\/\/monkeymoneyblog.com\/author\/fgarcia00\/"},"date":"Aug 31, 2025","dateGMT":"2025-09-01 00:29:58","modifiedDate":"2026-02-20 08:50:27","modifiedDateGMT":"2026-02-20 13:50:27","commentCount":"1","commentStatus":"open","categories":{"coma":"<a href=\"https:\/\/monkeymoneyblog.com\/category\/apps\/\" rel=\"category tag\">Apps<\/a>, <a href=\"https:\/\/monkeymoneyblog.com\/category\/cash-advance\/\" rel=\"category tag\">Cash Advance<\/a>, <a href=\"https:\/\/monkeymoneyblog.com\/category\/manage-money\/\" rel=\"category tag\">Manage Money<\/a>","space":"<a href=\"https:\/\/monkeymoneyblog.com\/category\/apps\/\" rel=\"category tag\">Apps<\/a> <a href=\"https:\/\/monkeymoneyblog.com\/category\/cash-advance\/\" rel=\"category tag\">Cash Advance<\/a> <a href=\"https:\/\/monkeymoneyblog.com\/category\/manage-money\/\" rel=\"category tag\">Manage Money<\/a>"},"taxonomies":{"post_tag":"<a href='https:\/\/monkeymoneyblog.com\/tag\/cash-advance\/' rel='post_tag'>cash advance<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/credit-card-advance\/' rel='post_tag'>credit card advance<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/emergency-funds\/' rel='post_tag'>emergency funds<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/fast-money\/' rel='post_tag'>fast money<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/financial-emergency\/' rel='post_tag'>financial emergency<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/financial-help\/' rel='post_tag'>financial help<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/income\/' rel='post_tag'>income<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/mobile-apps\/' rel='post_tag'>mobile apps<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/payday-loans\/' rel='post_tag'>payday loans<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/quick-loans\/' rel='post_tag'>quick loans<\/a>"},"readTime":{"min":13,"sec":23},"status":"publish","excerpt":""},{"id":3015,"link":"https:\/\/monkeymoneyblog.com\/apps\/cash-advance-apps-that-dont-use-plaid\/","name":"cash-advance-apps-that-dont-use-plaid","thumbnail":{"url":"https:\/\/monkeymoneyblog.com\/wp-content\/uploads\/2024\/10\/Cash-Advance-apps-that-don\u00b4t-use-plaid.jpg","alt":"Cash Advance apps that don\u00b4t use plaid"},"title":"Cash Advance Apps That Don\u2019t Use Plaid - 6 Great Power Alternatives","postMeta":[],"author":{"name":"Felipe","link":"https:\/\/monkeymoneyblog.com\/author\/fgarcia00\/"},"date":"Oct 21, 2024","dateGMT":"2024-10-22 03:48:03","modifiedDate":"2026-02-20 08:50:14","modifiedDateGMT":"2026-02-20 13:50:14","commentCount":"0","commentStatus":"open","categories":{"coma":"<a href=\"https:\/\/monkeymoneyblog.com\/category\/apps\/\" rel=\"category tag\">Apps<\/a>, <a href=\"https:\/\/monkeymoneyblog.com\/category\/cash-advance\/\" rel=\"category tag\">Cash Advance<\/a>","space":"<a href=\"https:\/\/monkeymoneyblog.com\/category\/apps\/\" rel=\"category tag\">Apps<\/a> <a href=\"https:\/\/monkeymoneyblog.com\/category\/cash-advance\/\" rel=\"category tag\">Cash Advance<\/a>"},"taxonomies":{"post_tag":"<a href='https:\/\/monkeymoneyblog.com\/tag\/apps-without-plaid\/' rel='post_tag'>apps without plaid<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/cash-advance-apps\/' rel='post_tag'>cash advance apps<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/finance-apps\/' rel='post_tag'>finance apps<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/instant-loans\/' rel='post_tag'>instant loans<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/mobile-payday-apps\/' rel='post_tag'>mobile payday apps<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/no-plaid-cash-advance\/' rel='post_tag'>no plaid cash advance<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/payday-loan-apps\/' rel='post_tag'>payday loan apps<\/a><a href='https:\/\/monkeymoneyblog.com\/tag\/quick-cash-apps\/' rel='post_tag'>quick cash apps<\/a>"},"readTime":{"min":20,"sec":29},"status":"publish","excerpt":"Discover the top cash advance apps that don\u2019t use Plaid, providing quick and easy access to funds without requiring Plaid for bank verification. Learn how these apps work, their features, and why they are great alternatives for fast financial solutions."}]

Cash advance apps have fundamentally changed how millions of Americans access their earned wages. What started as a niche fintech experiment in the mid-2010s has evolved into a market serving over 23 million users who need immediate access to funds they’ve already worked for.

I’ve spent the past six years analyzing digital financial products, reviewing hundreds of apps, and interviewing users about their experiences with early wage access platforms. What I’ve learned is that cash advance apps occupy a unique and often misunderstood space in consumer finance—they’re neither traditional loans nor simple banking features, and that distinction matters enormously.

These apps work by analyzing your bank account activity, verifying your income, and advancing you a portion of wages you’ve already earned but haven’t yet received. The advance is then repaid automatically when your next paycheck arrives.

Cash advance apps are most suitable for:

- Workers with consistent direct deposit income who face occasional timing mismatches between bills and paychecks

- People trying to avoid bank overdraft fees (which average $35 per occurrence)

- Those who need small amounts ($50-$300) to cover immediate necessities

- Individuals actively working to eliminate more expensive forms of short-term borrowing

Cash advance apps are generally not appropriate for:

- Anyone experiencing chronic income shortfalls where expenses consistently exceed income

- People seeking to cover discretionary spending rather than genuine emergencies

- Users without stable employment or regular direct deposit

- Those already struggling with multiple subscriptions or fee-based services they can’t afford

This guide provides comprehensive analysis of how cash advance apps function, the various types available, their true costs, and practical guidance for determining whether they fit within a responsible financial approach.

How Cash Advance Apps Work

Understanding the mechanics behind cash advance apps reveals both their utility and their limitations.

Income Verification and Bank Connection

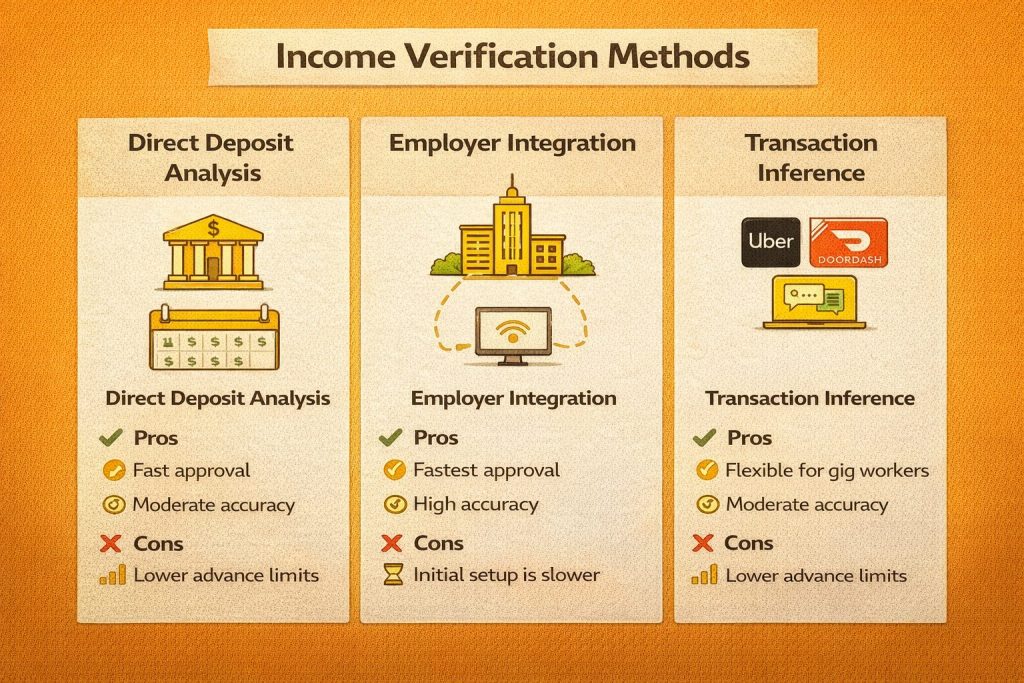

Cash advance apps must confirm that you have predictable income before advancing funds. They typically use one of three verification approaches:

Direct deposit analysis is the most common method. The app connects to your bank account and analyzes deposit patterns over several pay periods. It looks for consistency in deposit amounts, timing, and source. Most apps require at least 2-3 consecutive direct deposits before approving advances.

Employer integration represents a growing alternative where apps partner directly with employers. Companies like DailyPay and PayActiv work through employer payroll systems, giving them direct visibility into hours worked and wages earned. This provides more accurate real-time data than bank account analysis.

Bank transaction inference is used by apps serving gig workers or those with irregular income. These apps analyze incoming transactions tagged as income—whether from Uber, DoorDash, freelance platforms, or other sources. The verification is less precise, which typically results in lower advance limits.

Most cash advance apps use Plaid, an intermediary service that connects financial apps to bank accounts. When you “link your bank account,” you’re granting the app permission to access your account data through Plaid’s API. Plaid supports over 12,000 financial institutions, though credit unions and smaller regional banks sometimes lack integration.

The Plaid connection is read-only—apps can see your transactions but cannot move money without separate authorization. However, this access raises privacy considerations. Apps can see all transactions in connected accounts, not just income deposits. This means they have visibility into your spending patterns, other financial services you use, and overall financial behavior.

Repayment and Fee Structures

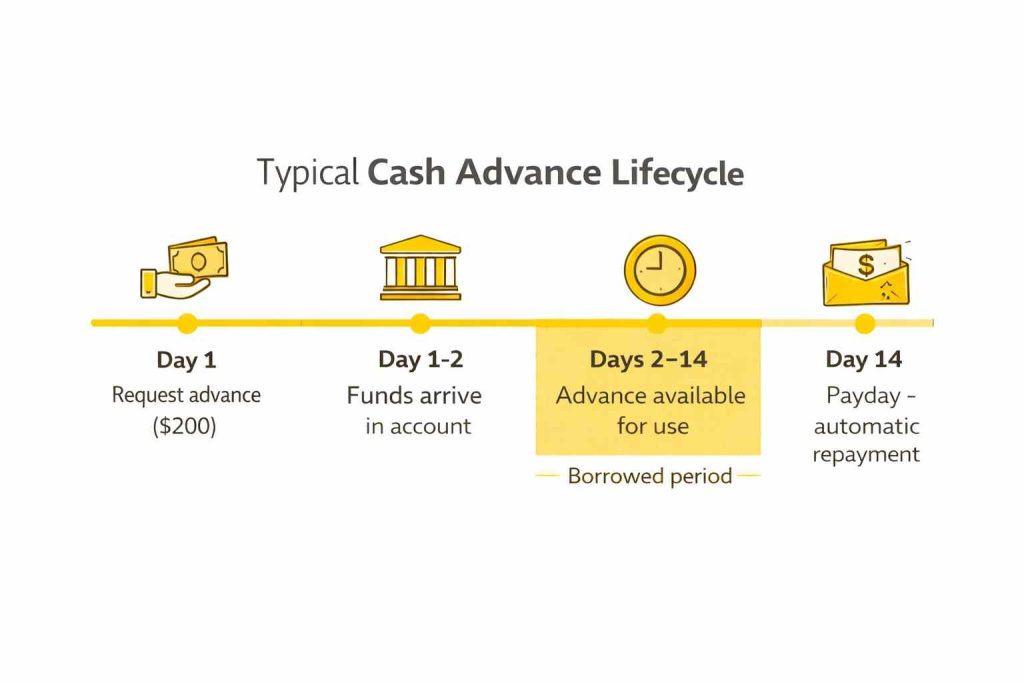

Repayment is where cash advance apps most clearly differ from traditional loans. Rather than negotiated repayment terms, these apps use automatic withdrawal on your next payday.

When you receive an advance, the app notes your next expected payday based on your deposit history. On or shortly after that date, the app initiates an ACH debit from your linked account. The exact amount advanced plus any fees is withdrawn automatically.

This automatic repayment structure is both the apps’ greatest strength and their primary risk. The strength: users don’t need to remember payments or actively repay. The risk: if your paycheck is smaller than expected or other bills hit first, the automatic withdrawal can trigger overdrafts.

Understanding fee structures:

Mandatory subscription fees: Apps like Brigit charge monthly subscriptions ($8-$14.99) that include advance access along with other features. The subscription is mandatory—you cannot access advances without it.

Per-transaction fees: Apps like Dave charge a flat fee per advance, typically $5-$15 depending on the amount. This model costs more per transaction than subscriptions but allows you to pay only when you actually need an advance.

Voluntary tips: Apps like EarnIn and Chime SpotMe use “optional” tipping models. Despite being “optional,” research shows the median tip is $5 per transaction—similar to mandatory fees charged by competitors. Interface design and social pressure create voluntary payment without mandatory fees.

Expedited transfer fees: Nearly all apps charge for instant transfers. Standard delivery (1-3 business days) is typically free or included in subscriptions, while instant transfers cost $1.99-$13.99 depending on the amount.

Key Differences from Payday Loans

Basis of transaction: Payday loans are true loans—you’re borrowing money you haven’t yet earned. Cash advances provide early access to wages you’ve already earned. The app is accelerating payment rather than lending new funds.

Cost structure: Payday loans charge interest as finance charges (typically $15-$30 per $100 borrowed, resulting in 300-400% APR). Cash advance apps generally avoid interest charges, instead using subscriptions, flat fees, or voluntary tips.

Repayment flexibility: Payday loans typically require full repayment on a specific date with expensive rollover fees if you can’t pay. Many cash advance apps offer repayment flexibility, extension options, or graduated repayment without additional penalties.

Collections practices: Payday lenders aggressively pursue collections and may take legal action. Cash advance apps generally limit collections to automatic withdrawal attempts and account suspension rather than aggressive collections.

Despite these differences, critics note that “voluntary” tips and expedite fees can approach payday loan costs when calculated as annualized rates. The regulatory perspective varies by state, with some explicitly excluding wage advance apps from payday lending regulations while others apply lending regulations.

Types of Cash Advance Apps

The market has diversified significantly, with platforms emerging to serve specific user needs.

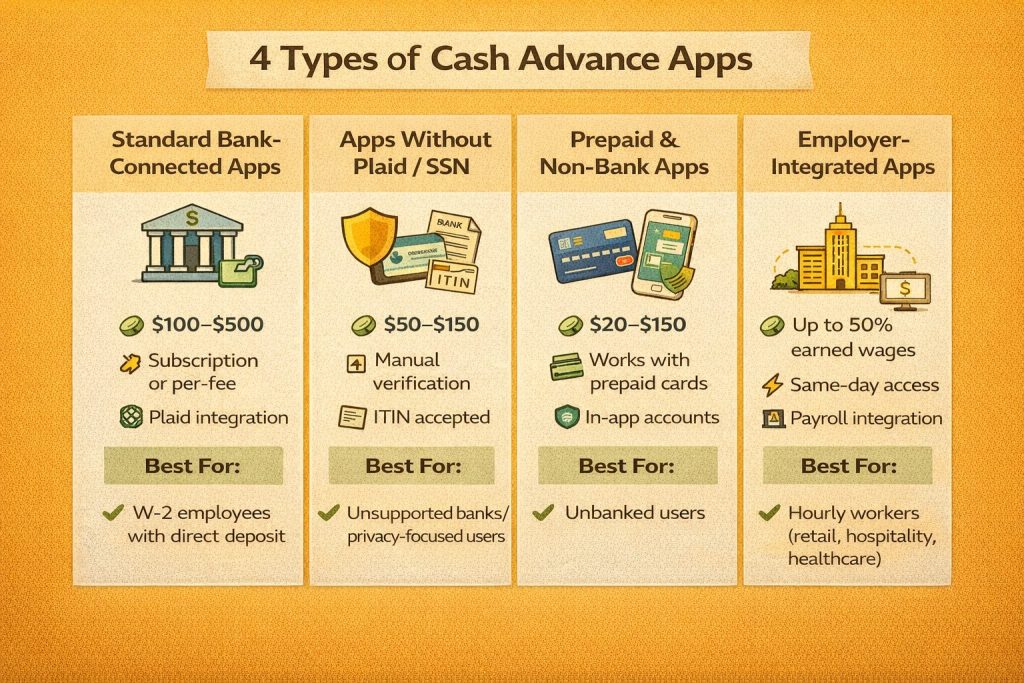

Standard Bank-Connected Apps

These apps use Plaid integration and direct deposit analysis to verify income. They typically offer $100-$500 advances with either subscription models ($10-15/month) or per-transaction fees ($5-10).

Best for: Regular W-2 employees with consistent direct deposit and supported banks.

Limitations: Requires compatible bank and stable income patterns.

Apps Without Plaid or SSN Requirements

Some apps use alternative verification methods including manual bank statement uploads, MX or Finicity connections (alternative aggregation services), debit card-based verification, or ITIN verification for workers without Social Security Numbers.

Best for: Users with unsupported banks, undocumented workers with ITINs, or those uncomfortable sharing SSNs.

Limitations: Lower advance limits ($50-$150), longer verification periods, more documentation required.

Prepaid Card and Non-Bank Apps

These apps work with prepaid debit cards, payroll cards, or mobile wallet accounts rather than traditional checking accounts. Some provide in-app FDIC-insured accounts, eliminating the need for separate banking.

Best for: Unbanked populations, those avoiding traditional banking.

Limitations: Higher fees ($5-15 per advance), lower limits ($20-$150), may perpetuate exclusion from mainstream financial services.

Employer-Integrated Apps

Your employer partners with the app provider and integrates it into their payroll system. The app has direct access to hours worked, wage rates, and earned but unpaid wages calculated precisely.

Benefits: Same-day access to earned wages, higher advance limits (sometimes up to 50% of earned wages), more accurate calculations, potentially employer-subsidized fees.

Limitations: Only works if your employer offers the program, access lost if you change jobs, potential privacy concerns with employer data visibility.

Best for: Hourly workers with variable schedules in retail, hospitality, or healthcare where these programs are common.

Understanding Costs and Risks

True Cost Analysis

The actual cost of cash advance apps depends entirely on usage patterns:

Light user scenario: One $100 advance every two months using standard delivery with no tips costs $0 annually.

Moderate user scenario: Two $100 advances monthly with $4.99 instant transfer fees costs $119.76 annually—approximately 60% annualized on $200/month advanced.

Frequent user scenario: Subscription model at $9.99/month for 3-4 advances monthly costs $119.88 annually—approximately 4% on $3,000 advanced.

Comparing to alternatives:

- Overdraft fees: Average $35 per occurrence—a single avoided overdraft pays for 3-4 months of app subscriptions

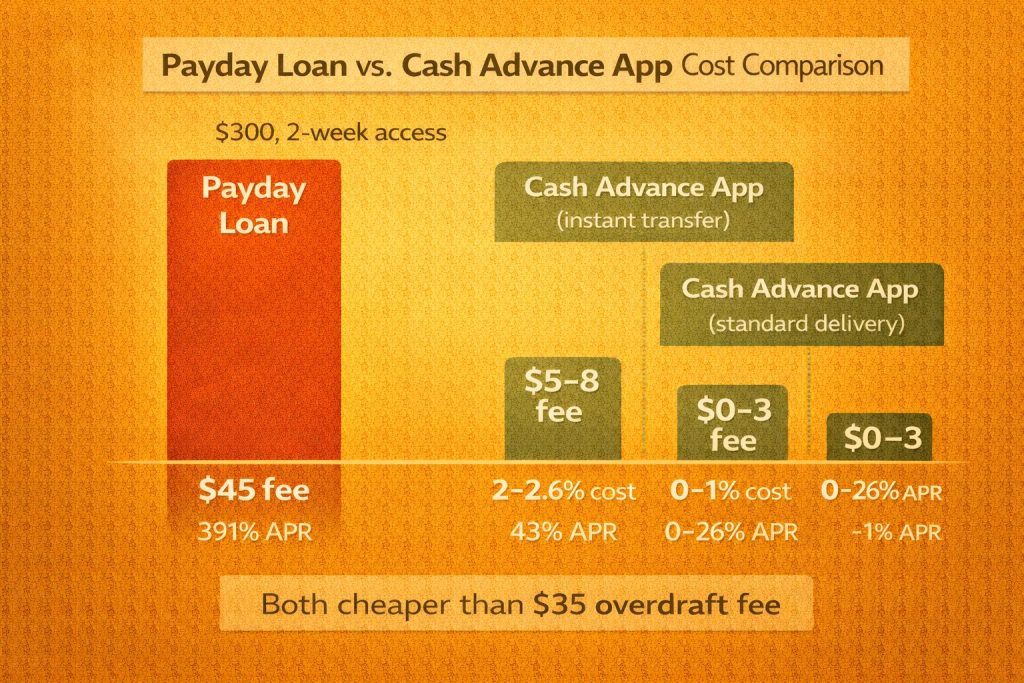

- Payday loans: Typical $300 payday loan costs $45 for two weeks—apps are 70-90% less expensive

- Credit card cash advances: 3-5% upfront fee plus 25-30% APR—apps are usually cheaper for small amounts

- Late payment fees: $25-$40 fees plus potential service disruption—apps can prevent these costs

Key insight: Cash advance apps are most cost-effective when replacing even more expensive alternatives, not when replacing proper emergency funds or budget adjustments.

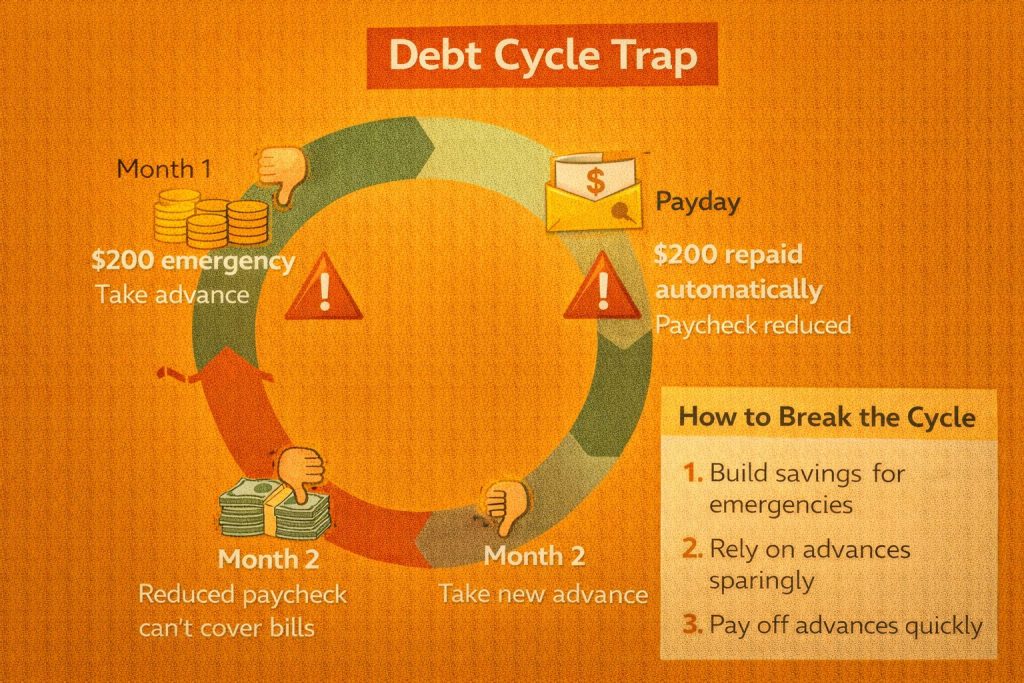

The Dependency Risk

The most significant risk isn’t explicit costs—it’s the potential for dependency cycles that mask underlying financial problems.

How dependency develops:

Month 1: Unexpected expense requires $200 advance. You repay from next paycheck.

Month 2: Next paycheck is $200 short because of repayment. You take another advance to cover normal bills.

Months 3-6: The pattern continues. You’re taking advances every pay period not for emergencies, but just to reach baseline budget. The advance has become part of regular cash flow.

Warning signs of dependency:

- Taking advances every single pay period

- Requesting advances immediately after previous repayment

- Gradually increasing advance amounts over time

- Using advances for routine bills rather than emergencies

- Feeling unable to “get ahead” of the advance cycle

Breaking the cycle: Take an advance “holiday”—choose one pay period to absorb the full paycheck without taking a new advance, even if it means cutting discretionary spending to near-zero. Create a micro emergency fund of $50-$100 to handle small emergencies. Address whether income actually covers expenses—if it doesn’t, advances can’t solve that structural problem.

Regulatory and Privacy Considerations

Cash advance apps are legal in most states but regulatory status varies. Some states apply payday lending regulations while others explicitly exempt wage advance apps. The Consumer Financial Protection Bureau monitors the industry but hasn’t issued comprehensive regulations.

Data privacy concerns: Apps collect extensive data including complete bank transaction history, employment information, personal identifiers, device and usage data. This comprehensive financial data creates risks including:

- Data breach exposure

- Third-party sharing with marketing partners

- Persistence even after stopping app use

- Identity theft risk from combined banking and personal data

Mitigating risks: Use dedicated accounts for paycheck deposits only, review privacy policies, enable available privacy controls, audit which apps have bank access regularly, use credit monitoring to detect unauthorized use.

When Apps Become Harmful

Cash advance apps cross from helpful to harmful when:

- Enabling overspending: Advances allow continuing to spend beyond income, masking unsustainable consumption

- Creating debt cycles: Taking advances to cover previous repayments mirrors payday loan traps

- Obscuring financial reality: Heavy use makes it difficult to know actual financial position

- Accumulating excessive fees: $30-50 monthly in fees ($360-600 annually) could build emergency funds instead

Clear warning signals: If you take advances every pay period automatically, amounts are increasing, you use multiple apps simultaneously, advance repayments cause other bills to go unpaid, you take advances for discretionary spending, or you couldn’t stop without immediate crisis—the apps are likely causing more harm than good.

Choosing the Right App Category

Comparison Framework

| App Type | Verification | Advance Range | Typical Costs | Best For |

|---|---|---|---|---|

| Standard bank-connected | Plaid integration | $100-$500 | $0-$15/month | Regular W-2 employees with consistent direct deposit |

| Non-Plaid/Non-SSN | Manual verification, ITIN | $50-$150 | $5-$15 per transaction | Unsupported banks, undocumented workers |

| Prepaid/non-bank | Debit card analysis | $20-$150 | $5-$15 plus card fees | Unbanked populations |

| Employer-integrated | Direct payroll data | Varies, often 50% of earned wages | $0-$5, sometimes employer-covered | Hourly workers in participating employers |

Selection Guidance

Step 1: If your employer offers an integrated program, start there (usually lowest cost, highest limits).

Step 2: Evaluate frequency of need:

- Rarely (once every few months): Per-transaction fee apps or tip-based with standard delivery

- Occasionally (1-2 times monthly): Calculate whether per-transaction or subscription costs less

- Frequently (3+ times monthly): Subscription models spread costs better—but also ask if you’re masking a structural budget problem

Step 3: Consider urgency patterns:

- If you typically need instant access, factor $3-8 instant transfer fees into cost comparison

- If you can plan 1-3 days ahead, standard delivery keeps costs minimal

Step 4: Check state availability and verify the app is properly licensed in your state.

Important warning: Using multiple apps simultaneously to access more cash than any single app would allow signals overstretching financially. This practice masks rather than solves underlying problems.

Frequently Asked Questions

Are cash advance apps legal in all states?

Cash advance apps are legal in most states, but regulatory status varies significantly. Currently, apps operate in 45-48 states, with restrictions in states that apply payday lending regulations. Before using any app, verify it’s available in your state and properly licensed. The regulatory landscape is evolving—state legislatures and the CFPB are actively studying these apps, and new regulations may emerge.

Do cash advance apps affect credit scores?

Most cash advance apps do not affect credit scores—neither positively through on-time repayments nor negatively through defaults. Most apps don’t report to credit bureaus at all. This means users with poor credit can access apps without credit checks, but successful use won’t help rebuild credit either. Some newer hybrid apps offer optional credit-building features with credit bureau reporting for additional fees.

What happens if I can’t repay a cash advance?

If repayment fails, apps will retry withdrawal 1-3 times (potentially triggering bank NSF fees). Your ability to request new advances is suspended immediately. After 7-30 days, your account is typically closed permanently. Most apps don’t report to credit bureaus, rarely pursue legal action for amounts under $500, and don’t garnish wages. Collections are generally less aggressive than traditional debt. Contact the app immediately if you can’t repay—many have hardship programs or payment plans.

Are cash advance apps safer than payday loans?

Cash advance apps are generally safer and less expensive than payday loans. Payday loans typically charge $15-30 per $100 borrowed (300-400% APR), while apps charge $0-10 per $100 advanced. Apps provide early access to earned wages rather than creating new debt, offer more repayment flexibility, and pursue less aggressive collections. However, both create dependency risks, and apps’ ease of use might make dependency patterns easier to develop.

Can I use multiple cash advance apps at once?

Technically yes, but this is almost always inadvisable. Using multiple apps simultaneously indicates overstretching—trying to access more money than you’ve earned. Multiple advances create compounded repayment burden, fee stacking, increased overdraft risk, and move toward debt-churning behavior. If you’re using multiple apps regularly, you’re likely masking structural budget problems rather than bridging temporary emergencies.

How do cash advance apps make money if some are “free”?

Apps generate revenue through: subscription fees (predictable recurring revenue), per-transaction fees, expedited transfer fees (70-90% margins), voluntary tips (60-70% of users tip despite “optional” framing), data monetization (anonymized financial data sales), cross-selling financial products (loans, credit cards, investment accounts), and employer fees (for workplace-integrated apps). “Free” apps aren’t charities—they have viable business models through data and product ecosystem monetization.

Conclusion

Cash advance apps serve as affordable bridges that help workers avoid overdraft fees, late payment penalties, and predatory payday loans. At their best, they provide occasional emergency access to earned wages at minimal cost. At their worst, they become crutches that mask structural budget problems.

The evidence suggests cash advance apps work best as occasional emergency tools for users with fundamentally sound finances, transition tools away from worse alternatives, and stopgap measures while building proper emergency funds. They work poorly as permanent cash flow fixtures, substitutes for budgeting, or solutions for chronic income shortfalls.

For users considering these apps, prioritize:

- Frequency: If you need advances every pay period, you’re treating symptoms rather than causes

- Amount: Consistently maxing limits signals need for fundamental financial restructuring

- Cost: If annual fees exceed $150-200, you’re paying enough to have built emergency savings

- Alternatives: Ask what you’re avoiding—if it’s “thinking about my budget” rather than “specific high-cost fees,” the app isn’t helping

The ultimate test: If using a cash advance app today helps you avoid using one next month, it’s working. If next month you need another advance to cover this month’s repayment, it’s failing—and you need to address the underlying issue rather than the symptom.

Cash advance apps remain useful tools when used appropriately—occasionally, for genuine emergencies, and as part of a broader plan to build financial stability. They become problematic when they replace that broader plan rather than supplement it.